Banks’ risk-based capital ratios remained stable and liquidity ratios continued to improve in the first half of 2021 even as the pandemic persisted, according to the latest Basel III monitoring results, published on February 21st. The report, published by the Basel Committee on Banking Supervision and based on end-June 2021 data, sets out the impact of the Basel III framework including the December 2017 finalisation of the Basel III reforms and the January 2019 finalisation of the market risk framework. It covers both Group 1 and 2 banks (see note to editors for definitions).

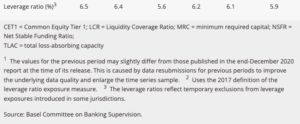

For the sample of Group 1 banks, risk-based capital ratios remained roughly stable, but leverage ratios decreased from the prior period. The largest decrease, of 1.1 percentage points, was seen in the Americas. This results from a significant increase in the leverage ratio exposure measure. Changes in exposure measures are in part driven by the end of temporary exclusions from the leverage ratio exposure measure. Several jurisdictions had put in place such exclusions during the Covid-19 pandemic.

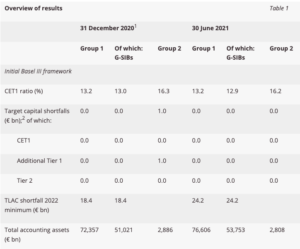

The final Basel III minimum requirements will be implemented by 1 January 2023 and fully phased in by 1 January 2028. The average impact of the fully phased-in final Basel III framework on the Tier 1 minimum required capital (MRC) of Group 1 banks is +3.3%, compared with a 2.9% increase at end-December 2020. Measures taken by some jurisdictions during the Covid-19 pandemic that reduce current capital requirements but leave capital requirements under the fully phased-in final Basel III standard unaffected could explain some of the observed increase in the impact. For this reporting date, Group 1 banks registered total regulatory capital shortfalls amounting to €2.3 billion, less than half that at end-2020.

The monitoring exercises also collect bank data on Basel III’s liquidity requirements. The weighted average Liquidity Coverage Ratio (LCR) increased to 144% for the Group 1 bank sample and to 225% for Group 2 banks. In the current reporting period, there are again seven Group 1 banks with an LCR below 100%. This is driven by banks using LCR reserves during the Covid-19 pandemic as intended by the framework. All Group 2 banks report an LCR well above the minimum requirement of 100%.

The weighted average Net Stable Funding Ratio (NSFR) increased to 125% for the Group 1 bank sample and to 130% for the Group 2 bank sample. As of June 2021, all but one Group 1 bank and all Group 2 banks in the NSFR sample reported a ratio that met or exceeded 100%.

The report is accompanied by interactive Tableau dashboards that allow users to explore the results with greater ease and flexibility. In addition to the credit risk and liquidity dashboards, an additional dashboard now covers the leverage ratio section of the report. Similar dashboards related to other sections of the report may be added at a later stage.

Source: BIS